By

·

3 minute read

By

·

3 minute read

Save Thousands by Re-Amortizing Your Loan with a Lump Sum Payment

The Effortless Way to Shrink Your Mortgage Payments

There's a method to pay off your home mortgage years sooner, while slashing interest costs, without the hassle of refinancing. Sound too good to be true?

It's a reality through a simple process called mortgage recasting. By making a lump sum payment towards your loan principal, your lender reamortizes the debt over the remaining term with the same interest rate.

The result? Smaller monthly payments that can save you thousands. Here's a closer look at this low-effort, high-impact mortgage tip.

How Does Mortgage Recasting Work?

The Lump Sum Payment

To recast your mortgage, you'll need to make a sizable lump sum payment towards the principal balance, typically a minimum of $10,000 or a percentage of the total principal. This large upfront payment immediately reduces the amount you owe on your home loan.

Keep in mind that this normally needs to be a lump sum payment, not an accumulation. The common advice of making a full mortgage payment every two weeks would likely not meet this criteria, and you could miss out on huge benefits.

Reamortization by Your Lender

Once you've made that lump sum contribution, your lender will re-calculate the amortization schedule - that's the breakdown of your remaining monthly payments over the loan's remaining term.

The requirement for fully-amortized loans is to reach $0 balance exactly at the end of the mortgage term, while maintaining a steady required monthly payment. With a lower principal balance, you'll owe less interest each month, resulting in a lower overall payment amount.

Servicer Fees

While much cheaper than refinancing, most lenders do charge a modest fee for recasting your mortgage, often around $250-$500. This small price covers the administrative costs of revising your loan.

Advantages of Recasting vs. Refinancing

When you recast instead of refinancing, you maintain your existing mortgage's term and interest rate - two key advantages over a traditional refinance. There's also no need for credit checks, home appraisals or other qualifying hoops to jump through. The process is simple, fast and much more affordable than refinancing.

Keeping Your Low Interest Rate

One of the biggest perks of recasting is being able to keep your original mortgage's interest rate, even if current market rates are higher. With a refi, you'd have to accept the going rate - which could erase any potential interest savings.

Avoiding Closing Costs and Red Tape

Refinancing often requires paying thousands in closing costs like appraisal fees, title searches and more. Recasting skips this expense, as well as a potentially lengthy underwriting process - saving you both money and headaches.

Retaining Your Loan Term

With a recast, your mortgage's existing term remains intact. If shortening or extending your payoff timeline is a priority, however, refinancing would allow you to adjust your loan's length.

Who Can Benefit from Mortgage Recasting?

Recasting is ideal for disciplined borrowers who have access to a substantial lump sum, whether from the sale of another property, an inheritance, work bonus or any other method of savings. It's a particularly appealing option if you want to pay down your mortgage faster without increasing monthly cash flow obligations.

Conventional and Jumbo Loan Holders

Unfortunately, government-backed loans like FHA, VA and USDA mortgages are not eligible for recasting under current guidelines. But if you have a conventional or jumbo mortgage, you're likely able to recast with your lender.

Borrowers with Home Equity

Most lenders require you to already have a certain amount of home equity built up before allowing a recast. This helps protect them in case you need to sell soon after. Check your lender's equity level requirements to ensure you meet the minimum.

Consistent On-Time Payers

Your payment history will also be evaluated. Many lenders require a history of consecutive on-time payments before approving a recast request.

Example of Best Use:

Let's put some easy numbers to use in an example, exaggerated to show effect.

Imagine your monthly payment is $1,000, and your budget has been setting aside $400 monthly to build up to recast. Total budget of $1,400 with them combined.

If it takes $10,000 lump sum, and $500 servicing fee, it would take you 27 months to build up those funds.

Now your payment may be $900, results vary so remember this is an illustration.

Your budget hasn't changed from the $1,400, so now it's $500 building up to recast.

You reach that $10,500 point in 21 months now. Let's say it saves you another $100.

$600 a month gets you to recast in 18 months. Meanwhile you've dropped an extra $20,000 off of your mortgage balance in 4 years.

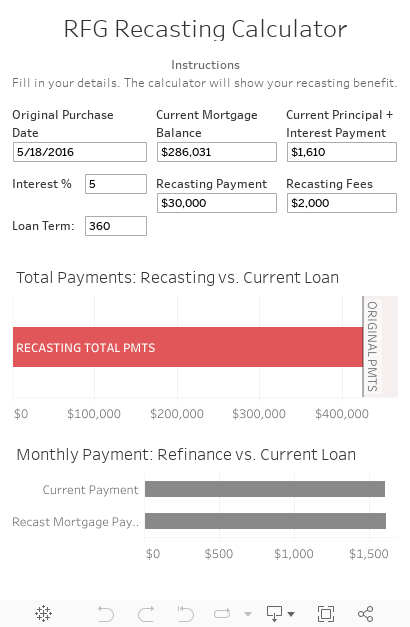

Want to test it out? Try this calculator to see the difference for yourself. Remember to only put in your Principal & Interest payment, leave any Escrow accounts out.

For homeowners fortunate enough to have funds available, recasting is an easy and cost-effective way to take chunks out of your mortgage balance while lowering monthly dues.

By avoiding the fees and hassles of refinancing, you keep your existing rate and term - a win-win for diligent borrowers.

If the criteria fits your situation, recasting could be a savvy move towards mortgage-free living. Especially if you repeat the process and hold your budget steady.